Dave & Buster's reports Q4 FY2025 earnings tomorrow and Polymarket is asking one question: Will PLAY's non-GAAP EPS come in above $0.46?

The Street thinks it'll earn around $0.38, so this isn't asking whether Dave & Buster's beats expectations. It's asking whether it beats by $0.08, which is roughly 21% more than anyone forecasts.

The market currently says that happens 21% of the time. The data says it's closer to 15%.

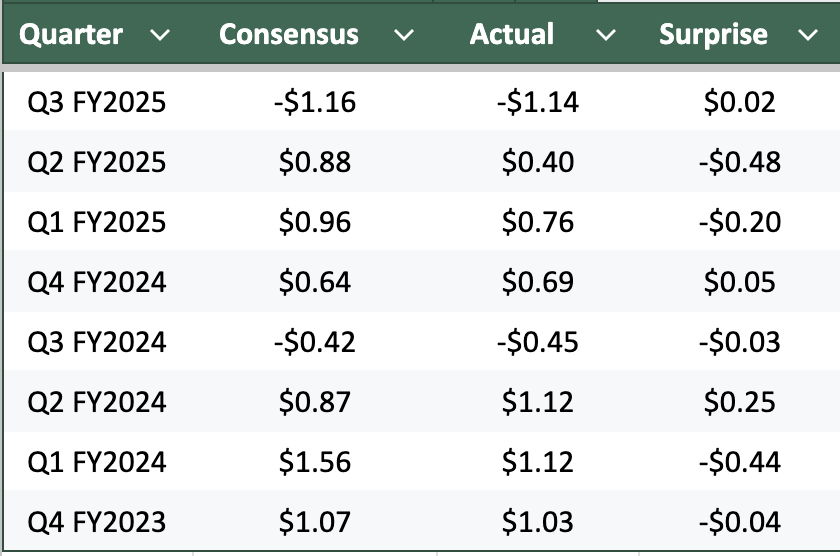

Eight Quarters of Evidence

Here's what PLAY has actually done over the last two years:

They've beaten estimates three times out of eight. They've been beaten by more than $0.08 exactly once, in Q2 FY2024, 18 months ago. In the five quarters since, the biggest upside surprise was +$0.05.

That's the base rate problem. History says the real probability of clearing this bar is around 12–15%. Polymarket is pricing 21%.

One more thing: five analysts cut their estimates after Polymarket created this market. The $0.46 bar was calibrated to an older, higher consensus, but the hurdle on Polymarket doesn’t move down with them, they keep it static.

Why the Bull Case is Real but Thin

The company is showing some positive signs.

Same-store sales improved from -9.4% in Q4 FY2024 to -4.0% in Q3 FY2025 and the holiday quarter is their peak for foot traffic.

A new menu launched in October had positive results and pushed food and beverage comps into positive territory. CEO Tarun Lal's "Back to Basics" plan, which included restoring TV advertising, simplifying promotions, and cleaning operations, is moving in the right direction.

Will Dave and Buster's Entertainment (PLAY) beat quarterly earnings?

Yes 19% · No 81%

Why the Downside Risk Compounds Fast

The economy is not helping them because consumer spending is softening.

The U.S. added 181,000 jobs in 2025, which is the slowest pace since before the pandemic.

Personal savings rates fell to 3.6%, the lowest since October 2022 and about 40% of consumers say they're cutting restaurant visits.

The lower-income customers tend to pull back on the restaurant and entertainment spending the most.

The balance sheet makes every miss hurt more. PLAY carries $1.59 billion in debt, a debt-to-equity ratio near 10x, and an interest coverage ratio of 1.3x.

S&P downgraded them to B- in September 2025. Fixed debt costs don't adjust, so every dollar of missed revenue flows straight through to their EPS number.

Q3 net loss was $42.1 million; one of the major reasons is that food costs are running 35% above pre-pandemic levels due to tariffs.

UBS also cut its price target to $13 in late March 2026. As you can see, they are facing some major headwinds to have one of their largest upside surprises in a long time.

Bottom Line

The $0.46 bar sits $0.08 above the expert’s consensus of $0.38. Getting there requires beating expectations by 21%, something PLAY has done once in two years and zero times in the last five quarters.

The market prices 'Yes' at 21%. The real number is closer to 15%. That's 6 cents of edge per dollar on 'No' at 79 cents.

The scenario where 'Yes' wins requires a huge holiday traffic surge and operating leverage, all arriving at the same time, while a consumer is pulling back and a balance sheet with quite a bit of debt. It can happen, but more like 1 in 7 times, not 1 in 5.

Bet 'No.' Size it conservatively.